If it wasn’t already clear, the writing is now well and truly on the wall for the fossil car makers: Just a week after BYD launched its $US15,000 “Corolla killer” and with the world’s largest EV battery maker recently announcing it’s on track to cut battery costs in half this year, new research suggests the decline in EV prices may by happening faster than thought.

Analysts think ICE (internal combustion engine) car makers are in for a rude shock, as EV prices come in below existing petrol and diesel models at the lower end of the market.

“EVs will soon be cheaper than ICE vehicles in the lower mainstream automotive market.” says Vision Mobility consultant James Carter.

“For the last few years, EVs have been more expensive than their ICE equivalent, particularly below US$40,000. However, what is extremely important to note is that battery prices, particularly for LFP [lithium iron phosphate], will continue to fall.

“Why? Because key minerals needed for LFP battery production are cheap: Lithium, iron, aluminum, graphite and copper. None are rare, all are commodity items and easily sourced from ethical supply sources. Even the lithium is cheaper as it uses lithium carbonate, rather than lithium hydroxide.”

Carter’s predictions are backed up by a new study by the International Council on Clean Transportation (ICCT) which has found that US lithium supply will outstrip demand (in the form of EV batteries) by a staggering three to one, further accelerating battery cost reductions and therefore EV prices.

The ICCT study uses EPA (Environmental Protection Agency) multi-pollutant standards which forecasts EV uptake at 67% of all US new vehicle sales by 2032 (up from 7% in 2023).

The analysis also assumes an average EV battery range of 300 miles (482 km). Based on these assumptions, the ICCT forecasts US lithium demand of approximately 340,000 tonnes per annum of LCE (lithium carbonate equivalent).

On the supply side, the ICCT says more than 100 lithium mining and refining projects are currently underway in the US and its existing and potential future FTA (free trade agreement) and CMA (critical mineral agreement) partners, which includes Australia.

Combined, these facilities are projected to produce 1,310,000 tpa of lithium extraction and 1,030,000 tpa of LCE in 2025. This is projected increase to 2,170,000 tpa of extraction and 2,040,000 of refined LCE by 2023.

With 2025 supply rates already outstripping 2032 demand rates by around 3:1, by 2032 the ICCT figures suggest LCE demand, in the form of US sold EV batteries will be just 17% of US and partner supply. The growing abundance of lithium suggests long term battery prices are set to continue to decline significantly for many years to come.

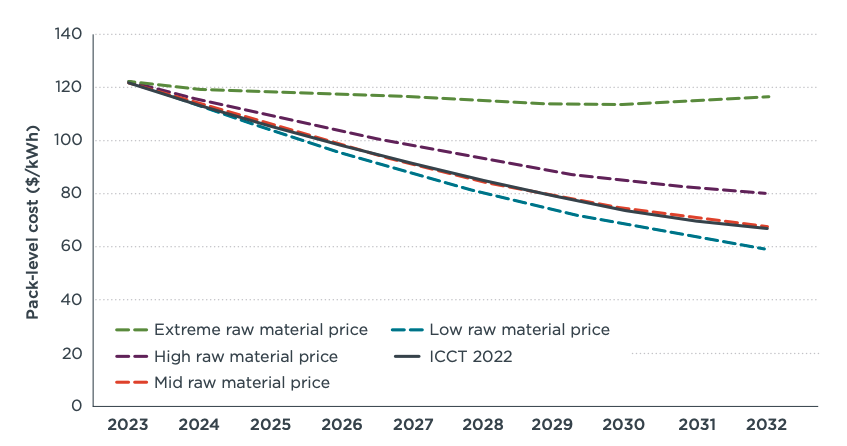

“Battery pack and BEV costs are linked to raw material prices, but substantial continued battery and BEV cost reductions are expected under most raw material price scenarios,” notes the ICCT report.

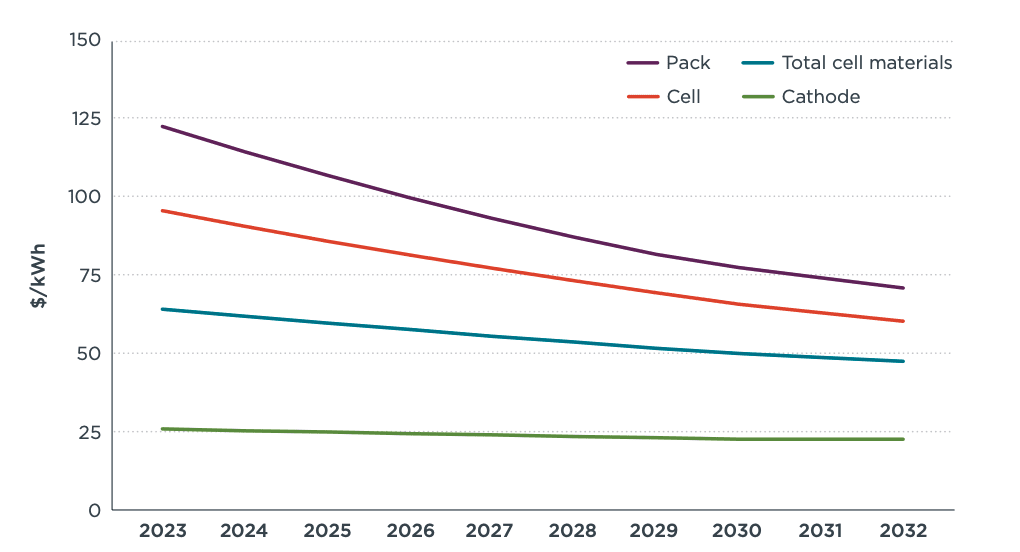

“Based on our “mid” raw material price scenario for lithium, nickel, and cobalt, which corresponds to a 50th percentile of historic prices, we find that battery pack costs decline from about $122/kWh in 2023, to about $91/kWh in 2027, and $67/ kWh in 2032.

“Under our 25th percentile “low” raw material price scenario, pack-level costs are reduced to $60/kWh in 2032”

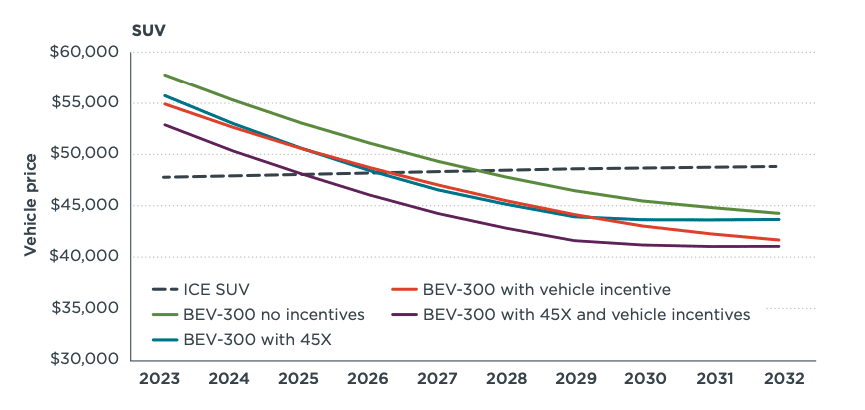

On that basis, the ICCT says: “We find that the upfront purchase prices of average new 300-mile range BEVs will be comparable to those of their gasoline counterparts in the 2028–2029 timeframe for cars, crossovers, SUVs, and pickup trucks without any government incentives.”

The ICCT report also found that the incentives from the US Inflation Reduction Act will accelerate EV new vehicle price parity with ICE vehicles by around three years.

“This study applies estimates of the average value of the Inflation Reduction Act Advanced Manufacturing Production Tax Credit (45X) for batteries and the Clean Vehicle Tax Credit (30D) for BEVs, which are estimated to be about $2,000 per vehicle for batteries and about $2,500 for new BEV purchases on average over the 2023–2032 timeframe,” it says.

“When both incentives are combined, they reduce the upfront BEV prices by up to $4,500 on average, which accelerates the timing for purchase price parity with conventional alternatives by about 3 years.”

That means, with the help of the IRA, fully electric SUVs will hit upfront price parity with ICE vehicles as soon as next year.

“When both the battery production and clean vehicle tax credits are considered, the 300-mile range SUV is expected to reach price parity with its conventional counterpart around 2025,” it says.

The new research, which suggests huge price reductions of all types of electric vehicles including SUVs and utes/pickups is in polar stark contrast to recent statements from the Australian fossil car lobby and its political representatives.

The CEO of the Federal Chamber of Automotive Industries (FCAI) Tony Weber recently threatened to launch a public fear campaign against the government’s proposed New Vehicle Efficiency Standard (NVES) saying it would cost Australian car buyers $39 billion, a claim which has been widely rejected.

The FCAI also recently released a list of vehicle price projections under the NVES which have been picked up and parroted by fossil backed politicians and media.

The projections assume EV market share, vehicle model efficiencies and model sales would stay the same in 2030 as they were in 2023, an absurd assumption based on current global trends.

In fact Australian vehicles use on average 20% more fuel than US vehicles, the shocking result of decades of failure to legislate vehicle emissions standards.

The absence of vehicle efficiency standards has turned Australia into a dumping ground for inefficient, expensive and highly polluting vehicles, something that’s benefited a small number of ICE vehicle makers and their political representatives but come at a huge financial and health cost to millions of Australians.

With EV running costs just a fraction of diesel and petrol cars and with the ICCTs new research showing EVs will be cheaper to buy than ICE vehicles in coming years, the fossil car lobby’s fear campaign is growing more absurd by the day.

Daniel Bleakley is a clean technology researcher and advocate with a background in engineering and business. He has a strong interest in electric vehicles, renewable energy, manufacturing and public policy.

Tesla's two door Cybercab - with no steering wheel or pedals - has been spotted…

NSW passes major milestone with more than 100,000 full battery EVs on the road. However,…

Tesla launches the FSD Supervised subscription offer in Australia and New Zealand, making the technology…

Tesla's most affordable models are now being produced with dozens of finished vehicles spotted at…

Tesla's first EV customer in Australia is not happy with treatment on FSD, amid reports…

Every truck we electrify and every ICE car we replace with a bicycle reduces our…

{kind=link}

{kind=link}

{kind=link}