“So what?” many people may ask about an overseas car awards list. What makes it interesting is the UK is a right-hand-drive, English speaking market with similar crash safety requirements AND is a lot further down the EV Transition track than Australia. As such, it provides a pointer to the near future of market trends here as well as what EV models could easily be sent to Australia – if manufacturers were willing to do so.

Where is the UK market currently at?

For the full year 2023, at 24% UK plug-in EV (PEVs) sales made up almost 1 in 4 new passenger vehicle sales. (BEVs – Battery Electric Vehicles – comprising more than two-thirds of that at 16.5%, with PHEVs – Plug-in Hybrid EVs at 7.4%).

Policy there towards EV adoption has (until recently) enjoyed bipartisan political support. This has resulted in long-term consistent policies that ensure a relatively smooth, well planned transition that includes all aspects of that transition.

These, by the way, include early passenger car price subsidies to encourage sales, medium to heavy trucking policies and support, standards for demand management of private EV charging and accessibility of publicly available chargers, interoperability of charger network billing systems … and the list goes on.

As an aside, an interesting blip occurred in the last month or so of the 2023 UK figures. Possibly due to the Conservative government’s recent back-flip on some EV policies – BEV uptake in the UK has slowed (but continued on a year-on-year upward trend) and PHEV/HEV sales have increased slightly. This could very well be a by-product of the public taking the ‘wait and see’ approach on future EV and emissions reduction policies, as suggested by surveys taken there since the changes.

So what are the interesting points in the What Car? list?

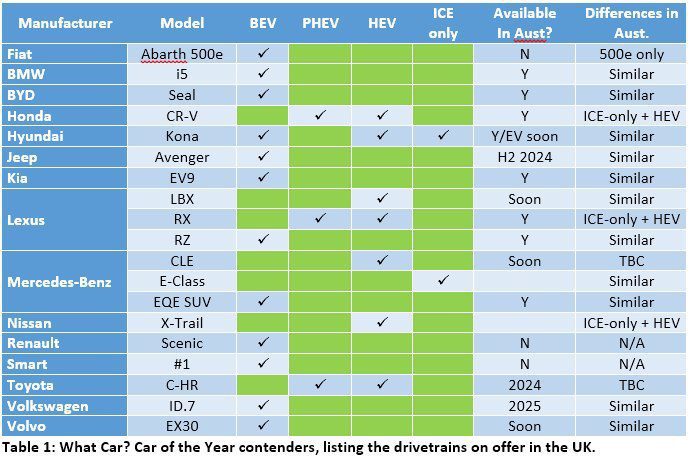

1. Of the list of 19 contenders for their top gong, 11 are BEV-only with the 12th (new model Hyundai Kona) the only multi-platform BEV. (It is available as BEV, HEV and petrol-only).

Of the others – three are offered there as PHEV or HEV only (no Internal Combustion Engine-only/ICE-only) and another three are HEV only. In fact, only one car on the list is offered as ICE-only: the Mercedes E-Class.

It would appear (for the UK at least) that in terms of notable vehicles for nomination, ICE-only vehicles are no longer seen as the leading edge in vehicle design or customer interest/benefit.

2. Of the 12 BEVs listed, only five are available here, such that you could drive away in one today. (Plus the base model of the Fiat 500e – we don’t get the Abarth version).

While several more are coming in 2024 or 2025, the delay is in no small measure due to our current lax to non-existent Australian Fuel Efficiency Standards (FES). Without these, there is simply no incentive for manufacturers to bring a greater range (or numbers) of BEVs to Australia as they gain far more benefit from selling them in markets that do have them.

3. Some of the model versions offered in the UK are different to Australia. Again due to the lack of an Australian FES, manufacturers are free to send their less fuel efficient models here. As examples: Honda Australia still offer the CR-V in ICE-only (not available in the UK) plus HEV, but not the PHEV that is offered in the UK. Same for the Nissan X-Trail and the Lexus RX.

So what might this say for our developing EV market?

It would be nice to say 2023 UK-like numbers in terms of BEV availability, interest and uptake will be seen here in two to three years’ time. (My crystal ball is, as ever, a bit hazy on exact timings. ;-).

How fast (or slow) our market progresses between now and when ICE vehicles are no longer available/only BEVs are made is, however, highly dependent on federal EV policy timing and strength.

- Timing: the longer the federal government delays a FES, the longer we will see fewer zero to low emissions vehicles offered, more fuel inefficient, high running cost ICE cars sold – and the longer these will stay on the road before they wear out and get replaced.

- Strength: many pundits have made the point that unless our FES is at least as strong as other OECD countries, we are likely to see a rise in PHEV and HEV availability and sales rather than of the least polluting BEVs.

Alternatively, if a strong FES is brought in ASAP, that two to three year trajectory could pick up speed – perhaps meeting the UK’s current numbers in as soon as 12 to 18 months.

My crystal ball is clear, though, on what a weak FES (or none at all) will do: ensure a slower uptake of zero-emission vehicles and make it even harder to reach our transport emissions reductions goals as we wait until the end of ICE production elsewhere, and we continue to wait for the ‘leftovers’ of overseas BEV markets to be sent here.

Bryce Gaton is an expert on electric vehicles and contributor for The Driven and Renew Economy. He has been working in the EV sector since 2008 and is currently working as EV electrical safety trainer/supervisor for the University of Melbourne. He also provides support for the EV Transition to business, government and the public through his EV Transition consultancy EVchoice.