Rising research and development costs for electric vehicles will put pressure on auto parts suppliers over the next few years, pointing to the need for automakers and their suppliers to ensure they are ready for the transition to electric mobility, a new report says.

Factors such as strict emissions regulations, battery prices, penetration of charging networks, as well as government policy and incentives will dictate the speed with which the transition occurs, and it is expected that electric vehicles sales will reach approximately 10 per cent globally by 2025.

But it how well OEMs and suppliers have readied for that transition which will have significant credit implications, and may dictate their future.

This outlook, which has been prepared by financial analysis company S&P Global, portrays a future for electric mobility that shows how dependent the success of transition will be upon a limited number of suppliers.

The transition will of course occur at different rates in different countries, with S&P Global saying that this is likely to happen faster in Asia, followed by Europe and then the US.

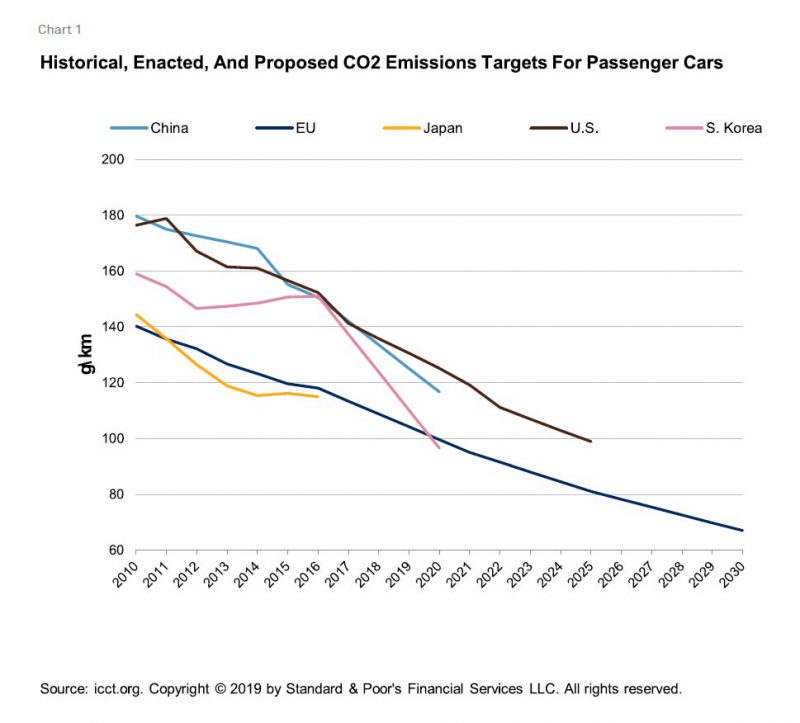

China is already leading the electric car market globally in terms of volume, with a plethora of Chinese automakers and EV startups well into electric drivetrain R&D and 1.26 million EVs sold in 2018 alone, up 61.7% from the previous year.

This is credited to its leading position on EV adoption policy, which demands an average CO2 emissions across its national fleet of 117gm/km, and offers a range of incentives from subsidies and lane access to drivers choosing to go electric.

Europe is likely to respond well in the near future with aggressive greenhouse reduction regulations to meet Paris Climate Agreement, says the report, aiming for 117gm/km average CO2 emissions by 2021, a further 15% reduction by 2025 and 37.5% reduction by 2030 for new cars.

It is also penalising new diesel vehicle sales among other measures, pushing the uptake to electric vehicles further.

In the US, policy is demanding an average fleet output of 95gm/km CO2 emissions, although S&P Global notes that the current Trump government has capitulated on previous emissions standards which demanded 5% of new vehicle sales by 2025 must be plug-in electric.

Also, it is believed that while 14 states – including the country’s leading EV market of California – have adopted their own standards, a disparate approach to EV adoption policy could both affect automakers’ decisions to decide firmly on ambitious EV investment.

This is especially the case if the disparity results in a split approach with a camp of states with stricter policies head to head against those with looser regulations.

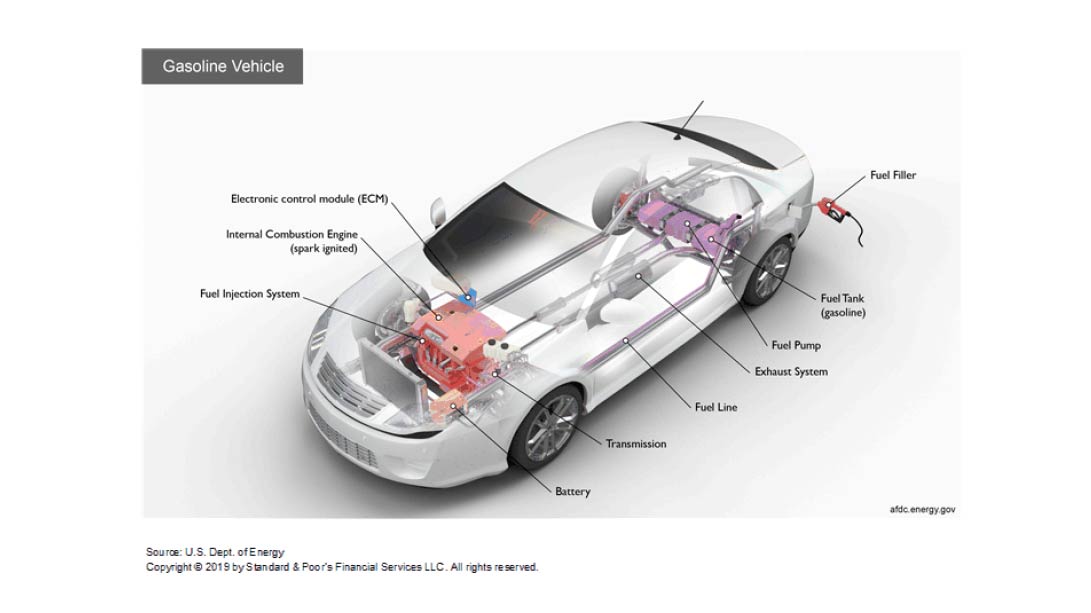

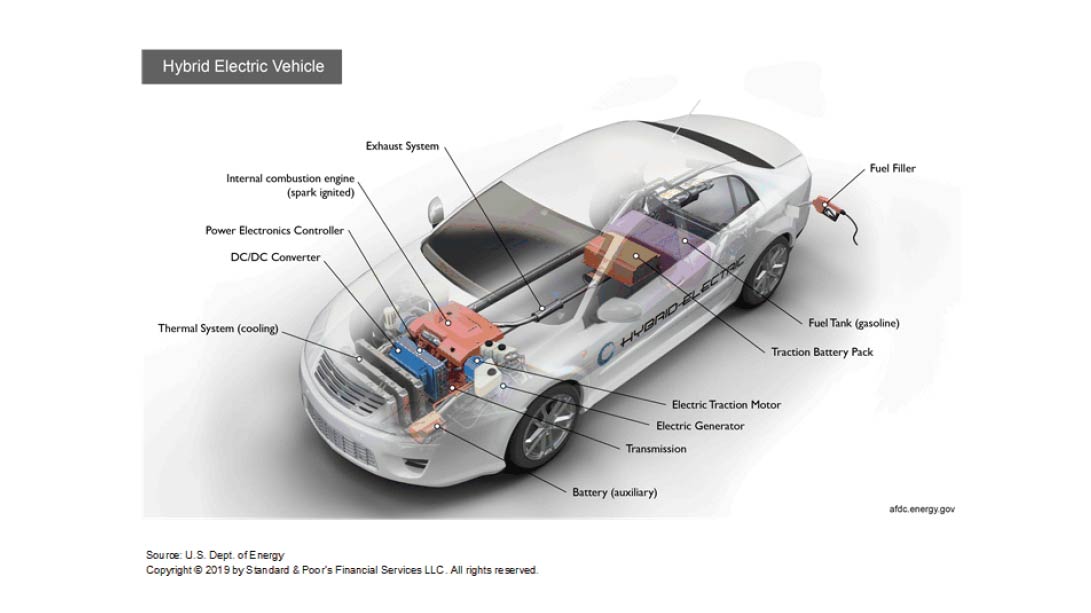

There is also the issue of automakers using plug-in hybrids to bridge the R&D gap, investing less in EV drivetrains and relying on existing ICE tech to comply with CO2 emissions regulations.

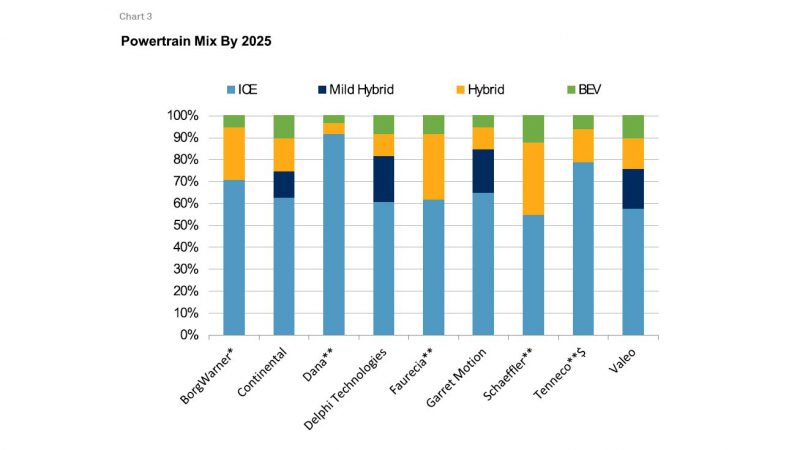

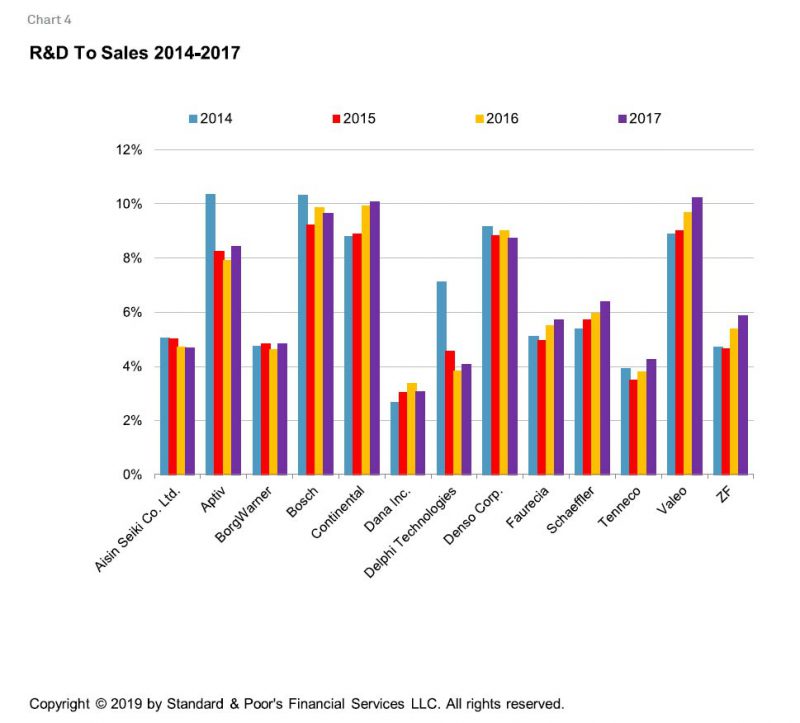

Surveying the current global EV market, S&P Global have assessed the state of play for 13 major auto parts suppliers – Aisin Seiki Co, Aptiv, BorgWarner, Bosch, Continental, Dana, Delphi Technologies, Denso Corp., Faurecia, Schaeffler, Tenneco, Valeo and ZF Friedrichshafen AG – and what the EV transition may mean for them.

For the purposes of this article, we’ve broken down the 13 suppliers according to S&P Global’s forecast outlook – namely, the good, the in-between and the bad.

The Good

It makes sense to consider Bosch first; it is the leading auto parts supplier, which generated €47.4 billion ($A75.8 billion) in revenue in 2018 from drivetrains, chassis systems control and electrical drives.

While it has recently signed a strategic with China’s answer to Tesla, Nio, it also has significant investment in gasoline and engine tech, which S&P Global says places it well to remain competitive over the next 10 years.

BorgWarner produces a full range of EV architecture, from pure electric drivetrain tech, as well as a number of hybrid architectures. It also has a number of products aimed at improving the efficiency of ICE vehicles but estimates that by 2023, one-third of its revenue will come from hybrid and electric technologies. This places it well in the changing auto supply market.

Although Denso attributes 45% of its revenue to Japanese carmaker Toyota (which continues to advertise its hybrid vehicles as “self-charging” much the the chagrin of the EV community), it does have a track record in developing electric and plug-in hybrid tech as well as supplying to a number of other OEMs. New business in autonomous technologies also place it as a candidate that will do well in transition to future mobility.

Faurecia has about a quarter of its hand in the anti-pollution pie for ICE vehicles, which as S&P Global says will be a liability in a transition to zero emissions mobility.

However, this kind of tech will still be required for hybrid vehicles for some time to come, while it hedges its bets on the FCEV market with the goal to halve the cost of fuel cell stacks. A long standing relationship with OEMs also places it well as a “credible supplier”, says S&P Global.

ZF Friedrichshafen AG, a global leader in drivetrain and chassis tech, already supplies a large range of hybrid and plug-in hybrid transmissions as well as EV drives.

With a recent €12 billion ($A19.2 billion) in R&D and capex slated for EV and autonomous driving tech over the next five years, S&P Global consider ZF among the competitive players despite a potential for these investments to tie up cash flow.

Delphi Technologies also has a low risk strategy in place which includes provision of all-electric, hybrid and ICE products, while Dana, which provides axles, driveshafts, seals and gaskets and so on to a range of auto markets has recently been acquired by Oerlikon Drive Systems whose efforts in electrification and hybrid vehicle development will ensure its position in a competitive market.

Maker of electrical components, Aptiv, has been concreting its position in the autonomous and next-gen mobility tech space with acquisitions such as KUM and Winchester, and say it is on track to triple its electrification revenue to $1 billion by 2022.

The Inbetween

Tenneco is placed in the inbetween category because although it has been involved in numerous hybrid programs winning it 9 hybrid program awards in 2018, its lack of product portfolio has investors worried that it will not have the flexibility to capitalise on the EV transition.

Valeo, which has its fingers in four market pies – driving assist and comfort, powertrains, thermal systems and visibility systems, is a key supplier globally for 12V and 48V systems, and is counting on 18% of vehicles by 2026 to rely on 48V systems.

Although it is reporting a cumulative order intake of €10.8 billion ($A28.8 billion) for its joint venture with Siemens, a reported loss in 2018 followed by a smaller loss this year means it has some catching up to do.

The Bad

Japan-based Toyota affiliate Aisin Seiki derives 55% of its revenue from selling underbody and drivetrain-related tech including automatic transmissions systems to Toyota, and while this will remain a positive in the short term while plug-in hybrids continue to require such tech, in the long term S&P Global say that it may not be able to respond to the loss of transmission demand due to EV uptake unless it expands its lineup of EV motors and speed reducers.

With €44 billion ($A 70 billion) in revenue for 2018, Continental is the second largest supplier of automotive parts in the world, offering ICE, hybrid and EV powertrains. However, even though S&P Global says it is well placed across all three main propulsion systems, a need to invest heavily in R&D may see it under pressure until sufficient scale is reached.

Lastly, Schaeffler – which supplies mechanical parts mostly for ICE engines – is according to S&P Global behind the eight ball. Its strong exposure to ICE markets means it has a lot of catching up to do in an auto market shifting to electric mobility, and this could see it suffer unless it ramps up its electrified product offerings.

A similar report released today by IDTechX discusses the challenges some major automakers may face if they do not respond with strategies that address the changing auto market.

Citing a need to meet “peak ICE” and then the inevitable “peak EV” that will eventually follow, automakers who fail to reimagine their brands and answer to market demand may follow the likes of Kodak and VideoEzy.

In a world of rapidly changing technology, IDTechX identifies 6 key items in a checklist to success for a future in the electrified auto industry:

- Strong position in quite large EV growth markets such as construction, agriculture, mining, urban transport beyond cars, aircraft, boats, ships.

- Speed in going 100% pure electric.

- Autonomy leadership – creative application in new sectors as much as technology.

- Strong balance sheet (sorry Tesla).

- In fast growing EV sectors where China is never going to be the dominant regional market.

- Inside the massive, protected market of China which took a rare breather in 2018 with a 3% decline in car sales, its first drop since 1990, but still 28 million units compared to 17.27 million for the USA at number two.

Who will succeed, and who will fail? By all accounts, the next ten years will tell.