Forecasts sure do vary for the uptake of electric vehicles in Australia. Last year, according to official data, there were just 2,400 sales of EVs in the whole country, even as accumulated sales of EVs surged through the four million mark world-wide.

And just when will the EV market finally take off in Australia? Probably when there are more models available, and the upfront cost becomes more competitive with petrol and diesel cars – even if the running costs of EVs is already significantly lower (as our story about 70-year old Sylvia’s solo trip around Australia illustrated).

One institution that is getting ready for a huge uptake of EVs in the coming decade is the Australian Energy Market Operator, charged with managing the grid and keeping the lights on, and soon to be charged with, well, the charging of EVs in a co-ordinated manner.

The recent publication of Electricity Statement of Opportunities – which is AEMO’s 10-year forecast of demand and supply and a key planning tool – assumed a major uptake of EVs over the next 10 years, as this graph below illustrates.

By 2027-28, for instance, it assumes 650,000 EVs on the road in Australia, which points to an average 65,000 EVs sold each year until then – although the uptake is not expected to be linear.

That, though, will just be the start of it. By 2037, in its neutral scenario, AEMO expects the number of EVs on the road to total more than 5 million, which suggests an average of more than 400,000 sales of EVs a year in that second decade.

Remarkably, this is the second big increase in long term EV sales forecasts by AEMO/ As were reported at RenewEconomy back in April, AEMO effectively doubled its forecast uptake on advice from various industry analysts.

Now it has increased that forecast again, as this graph below illustrates – with the solid lines being the latest forecast and the dotted lines the forecast made in March – which, I repeat, was a doubling over the forecast for this time last year.

What’s interesting here is that it is not the “fast change” scenario that has significantly increased in the latest forecasts, but the “slow” and “neutral” uptake scenarios, suggesting that AEMO expects this to happen, to varying degrees, come what may.

AEMO expects the inflection point of becoming cost-competitive with petrol vehicles to occur in 2027/28, and after that the uptake will accelerate.

“By 2037-38, 5.5 million residential and commercial electric vehicles NEM-wide are forecast in the neutral scenario, based on analysis provided by CSIRO. And this translates, as the table above illustrates, to around 18TWh of electricity a year, or about 10 per cent of the National Electricity Market.

How is it going to manage that?

It all depends on how and when they are charged, AEMO says, which in turn will be influenced by the availability of public infrastructure, tariff structures, and energy management systems.

And the driver’s routine.

AEMO has outlined three different charging profiles based on different scenarios.

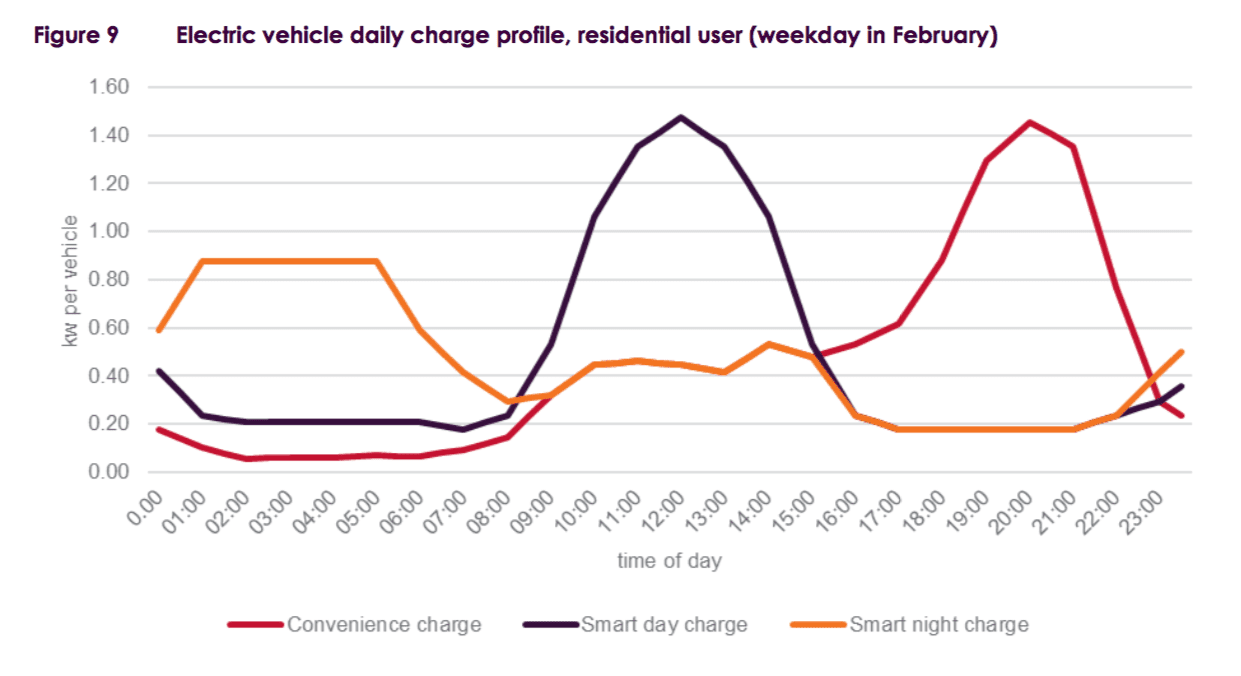

The first is what is known as “Convenience” charging – with vehicles being predominantly charged as soon drivers get home, including during peak hours.

- Then there is “Smart” day charging – with vehicles being predominantly charged in the middle of the day during the solar trough – the new phenomenon emerging in the grid where low demand and low prices shift from night-time to the middle of the day, thanks to the uptake of rooftop solar and the emergence of utility-scale solar farms.

- And then there is “Overnight” charging – with vehicles being predominantly charged overnight, after the evening demand peak.

- These are reflected in the graph below.

AEMO assumes that in the first years of solid EV uptake, it will mostly be convenience charging, which may add to peak demand, as the example residential charge profile in Figure 9 shows. (See the red line and how it adds to the peak in the evening).

AEMO assumes that in the first years of solid EV uptake, it will mostly be convenience charging, which may add to peak demand, as the example residential charge profile in Figure 9 shows. (See the red line and how it adds to the peak in the evening).

This reflects the absence of any incentive to optimise charging to manage demands on the power system, but as the uptake of EVs increases, AEMO hopes to see more retail tariffs or load controls that will manage the impact on peak demand.

AEMO flags that this may include changing regulation and tariff offerings and introducing technology that supports smarter charging.

“AEMO will review and adapt the charge profiles assumed for different users and the weighting of these as more data becomes available,” it says.

It also says that vehicle-to-grid technology (electric vehicles sending power back to the grid when connected at time of peak demand) has not yet been considered, and AEMO thinks that this would be minimal over the next 10 yeaers.

But it also notes that the kilometres travelled per vehicle could changes over time due to the adoption of car and ride sharing.

It says its assumptions are based around a battery efficiency at the start of the forecast period of approximately 1.1 kWh per km. Batteries toward the end of the forecast are assumed to become more efficient, requiring approximately 1.0 kWh per km.