Conditions are ripe for India to become one of the largest passenger car market in the world, says a report recently released by consultants McKinsey& Co..

Combined with policy plans and purchase decisions by Indian government at all levels geared at lowering emissions and reducing dependence on oil, this could mean that India is set to become a key player in the emerging global electric vehicle market.

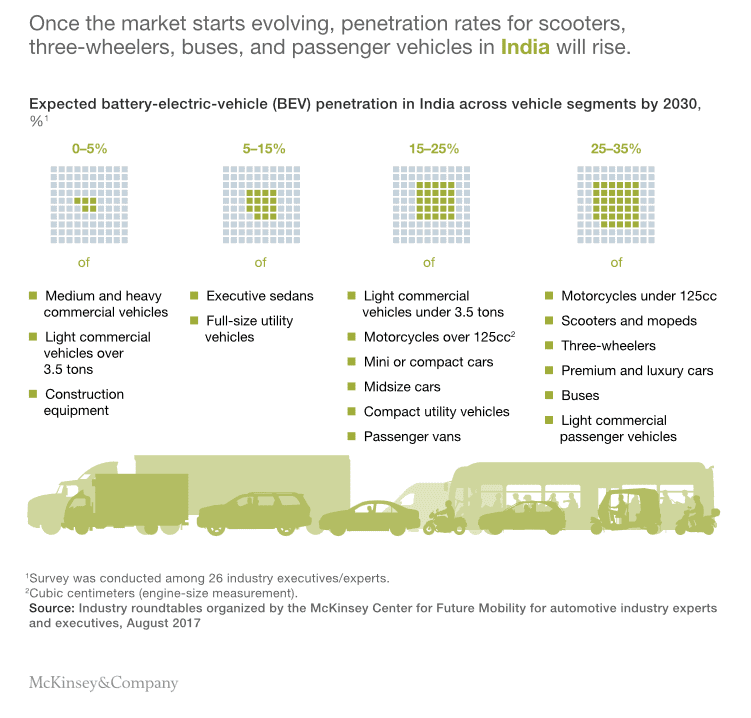

McKinsey says that India is already likely to reach high market penetration of two-wheeler and three-wheeler vehicles as well as premium and luxury cars and passenger vehicles by 2030.

Another report says that India will become the 3rd largest market of passenger vehicles by 2021, a figure backed up by the fact that while the country’s auto production went from 3 million to 4 million in the last 7 years, it is expected to reach 5 million within the next five.

Things are gearing up in India, in more ways than one.

Economic trends setting the perfect scene for higher rates of mobility include increasing urbanization, rising incomes and more people in the workforce, which at its simplest means more people who need to get around cities, with the disposable to either buy their own car or make more use of public transport schemes or disruptive options such as e-hailing (think Uber).

These trends are coupled with the introduction of several initiatives aimed at driving the buying choices of this new upwardly mobile sector towards low or zero emissions options, unlike in Australia (where policies to encourage the shift to zero emissions are currently lacking, although one would hope that with the Senate Select Committee on Electric Vehicles this will soon change).

For one, India’s National Electric Mobility Mission Plan (NEMMP) seeks to both encourage long-term growth in the local auto industry as well as reduce emissions and oil dependence.

Another, under the moniker of FAME (Faster Adoption and Manufacturing of Hybrid and Electric Vehicles), offers incentives to EV and hybrid car buyers such as a lower GST of 12 percent is applied to battery electric vehicles (compared with 31 to 48 percent for other vehicles).

An extension of that program (FAME2) has also introduced incentives for the electrification of public transport fleets such as buses and taxis, and encourages demand for all types of alternative fuel.

Ensuring that pollution from ICE vehicles are also dealt with, the Indian government is also looking at bringing in another initiative that will encourage adoption of end-of-life policies through lower taxes, discounts on EV purchase, and easy-to-follow compliance processes.

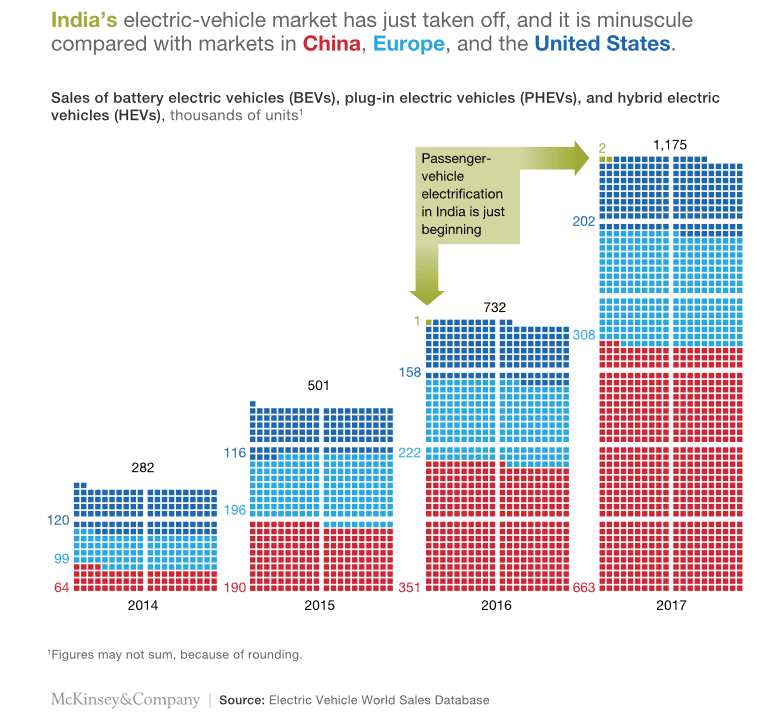

While the Indian market for EVs is still tiny compared to global leader in EV adoption including China, the US and Europe – only 2,352 electric vehicles were sold in India in 2017, compared with nearly 580,000 in China in the same period, there are moves by government to create a better environment for this to change.

One of the paths through which the country is addressing this is by working on improving industry by addressing parameters with its ‘Make in India’ strategy, to raise its ranking of 30th in the World Economic Forum’s global manufacturing index.

Government agencies are also embracing the shift to electrification of transport, with Indian energy service ‘Energy Efficiency Services Limited’ recently ordering 10,00 electric vehicles and local governments in 10 cities ordering 390 electric buses with the intent to buy 1,000 e-buses in a next phase of purchase.

Taking purchase decisions such as these into consideration with the fact that experts say people carriers like buses, two- and three-wheelers, luxury passenger vehicles, and light commercial vehicles could see maximum penetration in India by 2030, one can argue that it will be governments and commercial fleets that will drive EV market penetration.

However there are still barriers to this encouraging outlook, as the McKinsey report notes.

As in Australia, the lack of availability of EVs and commitment from local car makers to take up the flag for electrification – both incumbents and startups – will stifle any possible increases in EV adoption if not addressed.

India’s dependence on China for raw materials is also of concern according to the report, as is India’s inability to compete effectively in power electronics and battery manufacturing.

Additionally, there is a distinct lack on EV charging infrastructure in India, with only 1,000 stations currently in operation.

Along with the usual concerns of range anxiety and lack of education about the reliability and safety of EVs, there are clearly some issues to tackle in order for EVs to take hold.

All this aside, the incentives for the widespread adoption of EVS in India are inviting, such as the reduced total cost of ownership – all the more so because of the high number of possible applications where using cars forms the basis of occupation.

India is also known for its ‘frugal engineering’ methods, where cars are developed and made using lean and cheap methods to produce vehicles. One such example is the case of a mini developed by Indian engineers that was then sold for $5,000, reaching sales of 8,000 a month and 98% localisation.

With global auto players such as Ford cutting deals to work with local car maker Mahindra, to produce a new electric vehicle, India is clearly being recognised as one to watch for the shift to EV.

And they may just do it – by running lean, efficient operations, continuing to offer ‘Make in India’ incentives and both partnering and nurturing tech talent to make a serious bid to chase China as one of the world leaders in EV production.